News

January 29, 2024

Recent extreme hot and humid weather across Queensland has resulted in a new record level of electricity demand across the grid. Powerlink has reported that at […]

February 10, 2017

Australia’s power generation mix continues to evolve. Over a decade ago in 2006, the National Electricity Market (NEM) primarily relied upon electricity from coal-fired generation. Roll forward […]

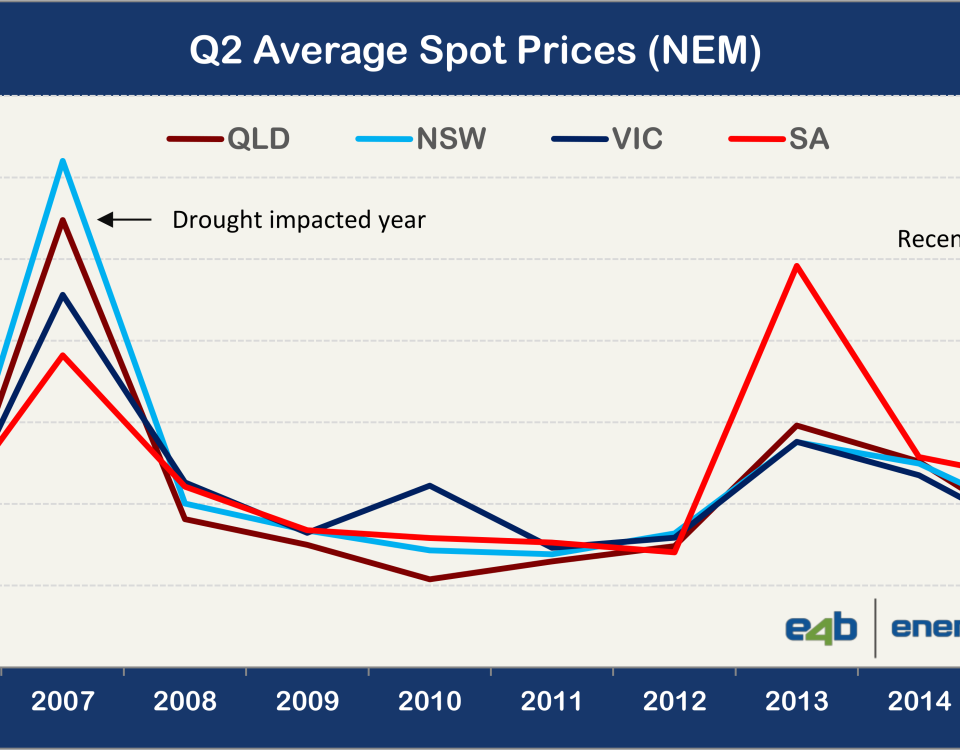

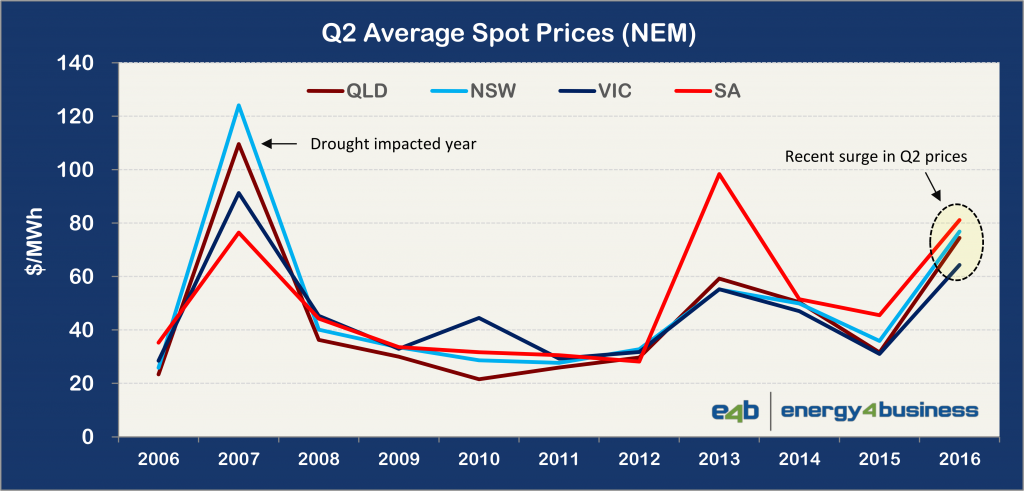

July 12, 2016

Businesses renewing their retail electricity contracts during the last quarter (Q2 2016) faced significant price rises due to a spike in forward wholesale electricity contract prices. These […]

November 6, 2015

Over the past decade there has been a very significant change in the sources of power generation used to supply electricity customers in South Australia (SA), […]

October 1, 2015

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The AEMC has called for public comment its draft determination to enable customers in embedded networks top choose their own electricity retailer. Embedded networks are privately-owned […]

July 10, 2015

The Australian Energy Regulator (AER) published SA Power Networks’ (SAPN’s) approved 2015-16 pricing proposal on 30 June 2015. This proposal contains the network tariffs that will […]